Property depreciation is a non-cash tax deduction available to the owners of income producing properties.

As a building gets older, items wear out – they depreciate. The Australian Taxation Office (ATO) allows property owners to claim this depreciation as a tax deduction. Depreciation on mechanical and removable plant and equipment items such as carpets, stoves, blinds, hot water systems, light shades and heaters are all valid deductions. There are also deductions available for the wear and tear of the structural element of a building, commonly called a capital works deduction.

Investors often wonder about the depreciation potential of older properties compared to new properties. The simple answer is that the owners of newer properties will receive higher depreciation deductions. However, all investment properties both new and old can attract depreciation deductions for their owners.

Newer properties have newer fixtures and fittings, so the starting value of those items is higher, resulting in higher depreciation deductions. The same applies to the capital works deduction. 2.5% of the structural costs of a building can be claimed per year for forty years. Construction costs generally increase over time, making building write-off deductions on new buildings higher.

Owners of older properties can claim the residual value of the building up to forty years from construction. For example, if an investment property is five years old, the owner will have thirty five years left of capital works deductions to claim.

Capital works deductions are governed by the date that construction began. If a residential building commenced construction before the 15th of September 1987, there is no building write-off available. Investors who own properties that are built before this date will still be able to make a claim on the fixtures and fittings within the property and include any recent renovations, even if the renovation was carried out by a previous owner.

It is always worth getting advice about the depreciation potential of a property regardless of age. The deductions are not as high on older properties but there are usually enough deductions to make the process worthwhile.

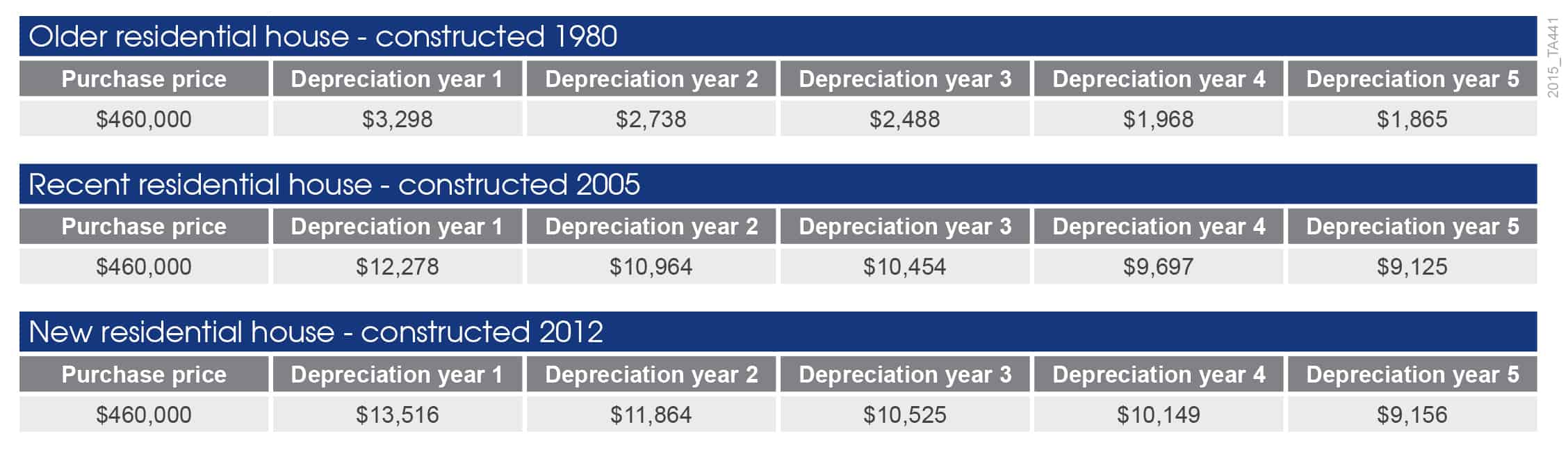

The table below shows the difference a depreciation claim can make for the owners of new, old and recently constructed residential house.

The depreciation deductions in this case study have been calculated using the diminishing value method. The depreciation found within properties of the same price and age can vary significantly depending on the property size and number of plant and equipment assets found in the property. Additional deductions may also apply if there has been any additional works or renovations completed.

As you can see, although the owner of a newer residential house constructed after 2012 will receive much higher deductions, the owner of an older house constructed in 1980 will still receive substantial deductions. In the first financial year alone they can claim $3,298 in deductions and over five years deductions total to $12,357.

Investors who would like more information about property depreciation can visit the BMT Tax Depreciation property investor’s page on their website by clicking here.

To obtain a free estimate of the deductions available in any investment property or for obligation free advice, investors can contact one of the expert staff at BMT Tax Depreciation on 1300 728 726.

Article provided by BMT Tax Depreciation.

Bradley Beer (B. Con. Mgt, AAIQS, MRICS) is the Chief Executive Officer of BMT Tax Depreciation. Please contact 1300 728 726 or visit www.bmtqs.com.au for an Australia-wide service.